Multimedia - Komisja Nadzoru Finansowego

COMMUNICATION

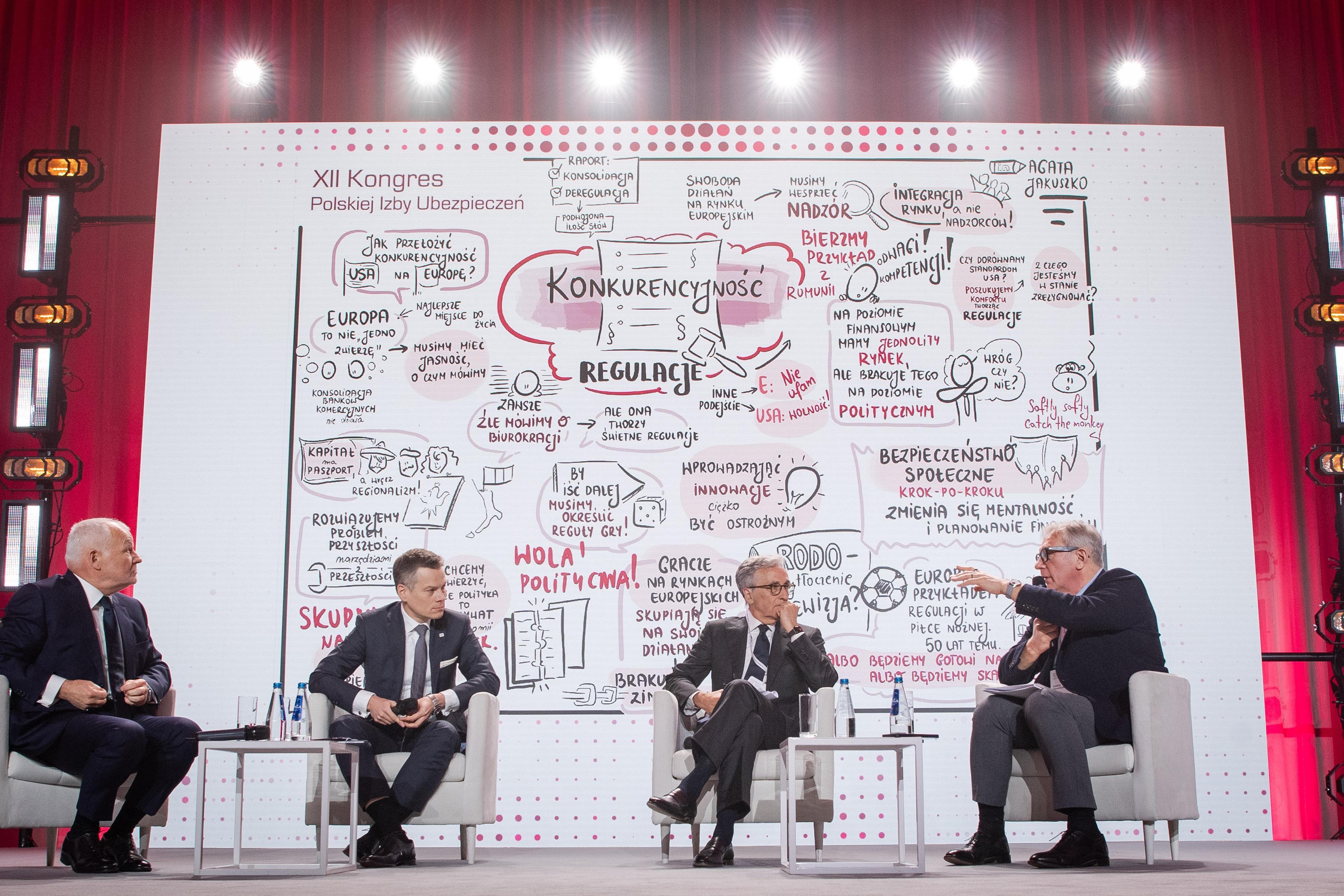

Jacek Jastrzębski spoke on the ‘Competitiveness – regulation’ panel at PIU Congress

Jacek Jastrzębski, Chair of the KNF, spoke on the ‘Competitiveness – regulation’ panel at the 12th Congress of the Polish Chamber of Insurance (PIU). The debate, moderated by Cezary Stypułkowski, CEO of Pekao S.A., was joined by Jan Krzysztof Bielecki, former prime minister of Poland, and Dr Vittorio Grilli, former minister of economy and finance in Italy.

Key points of Jacek Jastrzębski’s speech during the panel:

- One of the positive implications that the new U.S. administration may have for Europe is that we have clarity on some points and we are talking openly about some points that we haven’t had the courage to talk that openly before. One of these topics is the national interest and the role of national state in the economy. I consider this as some sort of a benefit that – because of the clear message we hear from across the Atlantic and we have to learn – we are talking openly about the role of the national security factor and the role of state factor in the economy, including in financial markets.

- As regards the freedom to provide services and the freedom of establishment in the context of the KNF’s supervisory activities, we should note that we are a relatively sizeable market. What we see in the European regulatory and supervisory landscape is that there are jurisdictions where the regulatory or licensing approach may be more relaxed, because they are licensing mainly for foreign markets. The KNF is regulating and licensing entities that to a large extent operate in our national market, so we are taking care of our customers. This affects our licensing and supervisory policies.

- Enhancing the supervision of cross-border activities, including the aspect of the freedom to provide services and the freedom of establishment, is one of the key topics that the European supervisory authorities should have a look at in the discussions around the integration of the financial market. It’s particularly true for insurance business because the motor third-party liability insurance is a particular product: a product you are buying, technically, for yourself to obtain the required insurance certificate, but someone else would be the beneficiary of the quality of this product. The moral hazard in this market is particularly acute. We had to resort to some sort of a nuclear scenario in connection with the activity of one of the foreign insurance companies operating in Poland, because it was a clear case where we saw that the business model developed within the freedom of services framework may be detrimental to the Polish market and it may distort competition in that market. It’s a clear sign that it’s an area we should be taking a closer look at.

- While talking about the integration of the financial market, I’m a big fan of talking about the integration of supervision rather than about the integration of supervisors. Integrated supervision does not necessarily mean integrated supervisors. And integrated supervision is particularly relevant in the context of cross-border activities, mostly in the field of capital market and insurance.

- The level of regulation is an outcome of some sort of a quest for equilibrium between comfort, safety, stability on one hand and progress and development on the other hand. That explains a lot because it’s true for the European area as a whole. In our quest for comfort, we have made certain decisions and we have reached such a stage of regulation where it has significantly impacted our ability to compete or to be profitable. The price that we are paying for this comfort is the difference that we see in the figures for Europe and for the United States.

- This quest for comfort is coming from many stakeholders: the public stakeholders, who after each and every crisis come up with regulations to prevent such a crisis from repeating itself in the future; the supervisors, who look for comfort in their daily activities, because regulations, including recommendations and guidelines, are the easiest way to respond to potential threats; but also business players, for whom regulations are some sort of a manual on how to run the business.

- The fundamental question is how much of this comfort we are willing to give up in order to become more competitive. That’s a question that everyone should ask, standing in front of the mirror: how much am I going to give up?

- Living in a world of overregulated financial market seems easier and safer. It will be better for the economy, though, to replace the regulatory approach or to supplement the regulatory approach with a more supervisory approach, because it’s more flexible. Supervision has the significant benefit of being more real-time. But it requires two factors: competence and courage.